Year In Review: Offshore Oil Services

Tidewater Puts The Team On Its Back, But The Best Is Yet To Come For Transocean, Valaris & Borr Drilling

Year In Review

We are getting towards the end of my Year In Review posts, and today’s will be focused on the offshore oil services sector. Tidewater TDW 0.00%↑ has been the big winner so far and is up well over 100% from my purchase price. It has singlehandedly carried the rest of the offshore basket over the last year. Transocean RIG 0.00%↑ has been volatile over the last year but it’s down a bit, while the Valaris VAL 0.00%↑ warrants are up slightly. Borr Drilling BORR 0.00%↑ has been the biggest loser so far, but in my opinion, it has the biggest disconnect between the share price and fundamentals of any stock in the offshore basket today.

Like the coal sector, I think we have a long way to go with this offshore cycle. Stocks in the sector are still trading at 30-50% of replacement cost (give or take), day rates across the sector continue to head in the right direction, and I think we are going to see meaningful capital returns from the sector in coming years. If I had to guess, I would say we’re in the third inning of this cycle, and I think the whole sector is going to deliver very good returns for investors over the next several years.

Changing Opinion on OSVs, Deepwater & Jackups

One of the things that has changed for me is my opinion on the different offshore oil services subsectors. Last spring, I was most excited about deepwater and Transocean. I thought they had the best deepwater fleet, and strong management that avoided bankruptcy in a vicious down cycle. This left them with a levered balance sheet and a ton of torque for an offshore bull market. All that still applies to Transocean, but I wasn’t paying enough attention to OSVs and jackups.

I was more focused on the irreplaceable nature of the deepwater assets (at least at current day rates and new build costs), and should have put more weight on the shorter contract duration for OSVs when making my buy decision on companies in the sector. That’s why Tidewater has performed the way it has, with their contracts quickly rolling over to higher day rates, and I think it’s going to continue.

The other thing I should have paid more attention to was the cold-stacked spare capacity for deepwater. This put a lid on day rates for a while, but it looks like we are going to start grinding higher this year. Later in the year, I started looking at Borr Drilling as I started to warmup to the jackup sector. Jackups are typically somewhere in between OSVs and deepwater as far as contract duration, but I think we are going to see day rates higher over the next couple years even if recent events in the Middle East mean that day rates are stuck in neutral for the near term.

Transocean

Transocean has been frustrating, especially over the last six months, but it has pretty much been a volatile ride to nowhere. I started buying Transocean last March and April, added shares and Dec 2026 calls this January. Those calls are up 10%, while my older (and smaller) batch of 2025 calls are down 80%. Similar to Peabody Energy BTU 0.00%↑, my calls on Transocean are a very small portion of my investment in the company.

I still think they have the best fleet and management, and I think we start to see their business gain momentum over the next year or two. My biggest mistake on this one was not selling the calls when shares had run hard last summer. I left a decent chunk of money on the table by not selling the 2025 calls, and I will be selling those at some point this year. I don’t plan on repeating this mistake if we get another run, especially with the small slice of December 2026 calls I bought earlier this year.

Average Cost Basis: $5.87

Current Price (as of 5/5): $5.55

Total Return through 5/5: -5%

Tidewater

Like I said earlier, I didn’t put enough emphasis on the shorter contract duration leading to a faster increase in cashflows for Tidewater. Despite the massive run over the last year, I still think we have a long way to go and I don’t plan on selling my shares any time soon. I was buying my shares last March, and the biggest mistake with Tidewater is not buying enough.

Tidewater’s run has me wondering if I should take a closer look at Seacor Marine Holdings SMHI 0.00%↑, which is a smaller operator of OSVs. I haven’t done enough digging to have an opinion one way or another, but I wouldn’t be surprised if it is along for the ride with Tidewater shares over the next couple years. As far as Tidewater, I think we are going to see more capital returns and a higher share price for long-term investors.

Average Cost Basis: $44.41

Current Price (as of 5/5): $106.90

Total Return through 5/5: 141%

Valaris Warrants

I was buying the Valaris warrants in late 2023, but I increased my position meaningfully a couple months ago in March. While I think Valaris shares are in for good run over the next several years, I find the warrants to be a more attractive risk/reward proposition. A little bit more risk with the potential for a very outsized reward. The warrants have been good for a whopping 3% return so far, but it’s still priced like a forgotten security.

Valaris recently signed a jackup contract at $145,000 day rates (approximately $200,000 per day including the mobilization fee) for two years in Angola. I will get into my rant on Borr in a moment, but it’s another reason I’m not worried about the market for jackups. This feeds into why I think the near term concern over day rates for Borr is overblown. As far as Valaris, I find the warrants to be the equivalent of a very long dated call option on an offshore bull market.

Average Cost Basis: $12.15

Current Price (as of 5/5): $12.51

Total Return through 5/5: 3%

Borr Drilling

Borr has been one of the most frustrating stocks in the offshore basket, because I think the gap between the share price and the actual value of the business has been getting wider over the last six months. I was buying shares in September through December, and made it a larger position in March. When I started buying there were a couple checkpoints I was looking for, and management has taken care of all of them. They started paying dividends, announced a buyback (we will have to wait until Q1 earnings to see if they have been buying back shares), and refinanced the debt to extend their maturities.

We have seen insider buying in recent months, and despite all of that, shares are down more than 20% YTD. I have been wrong on Borr so far, but I think the market is overreacting to short-term news and missing the forest for the trees. There have been multiple headlines since the start of the year that have led to selloffs, while the market reaction to signing contracts for three jackups at an average day rate over $193,000 sent the stock up 10 cents. That second part is going to have a much larger impact on Borr’s results than any of the negative headlines, even the release of one of Borr’s jackups by Saudi Aramco (which had a sub-$100,000 day rate by the way).

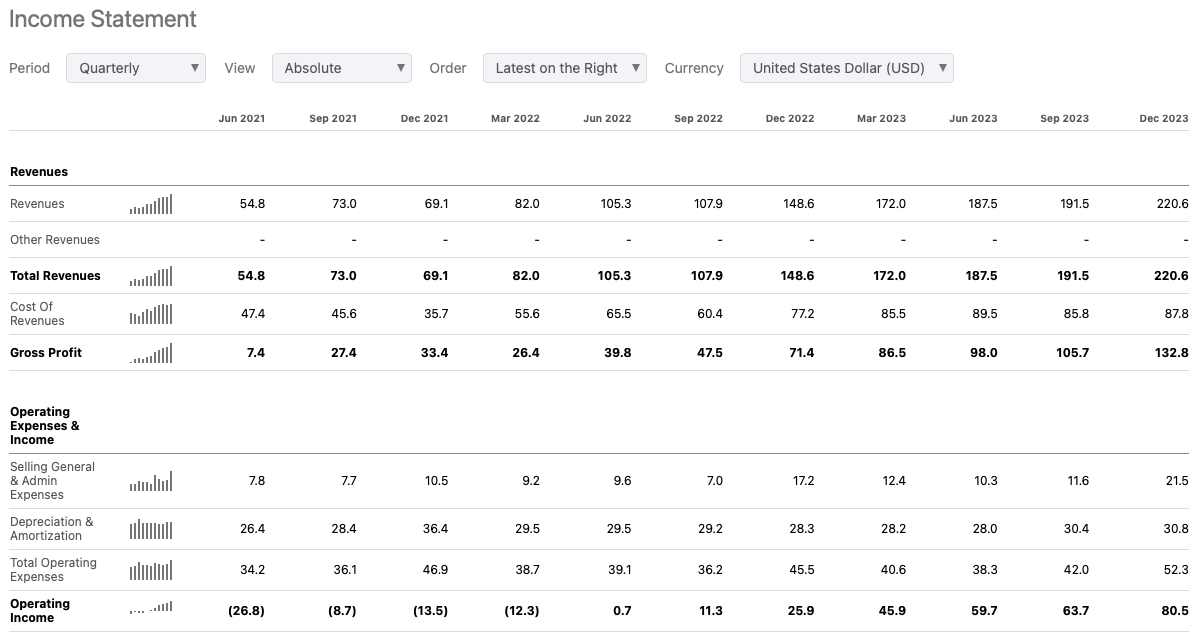

Day rates might be weak in the near term in the Middle East, but I’m not too worried about Borr’s exposure to that part of the world. The two jackups set for delivery by year end is another thing to watch for, but I’ll be doing a closer look at Borr once they report earnings later this month. I also wanted to drop a screenshot of Borr’s quarterly results over the last couple years just so readers can visualize what the business has been doing even while the stock has sold off. Eventually the share price will notice that trend of revenue and income up and to the right.

Average Cost Basis: $6.51

Dividends received: $0.05 per share

Current Price (as of 5/5): $5.54

Total Return through 5/5: -14%

Conclusion

The offshore sector has been a mixed back for me so far. It’s tough to hurry up and wait, but that’s the position I’m in right now. I can’t complain about Tidewater, but I think the rest of the basket follows along, albeit in a delayed fashion. Transocean and Borr have torque with their levered balance sheets, while the Valaris warrants have the torque built in. It’s a long cycle for offshore oil services, and we have years of runway left in my opinion. I’ll be wrapping up tomorrow with a review of all the other trades and holdings in the portfolio.

Disclaimer

I own shares of Tidewater, Transocean, and Borr Drilling. I also own calls on Transocean and Valaris warrants. You should do your own research before making any investment decisions. Different investment strategies have different risk/return profiles which should be considered before making any decisions.