Tidewater: The Dominant Player In An Offshore Niche

Rising Day Rates Will Drive Shares Of Tidewater Higher Over The Next Couple Years

Summary

Tidewater is the largest company focused on OSVs in the offshore sector. They have completed two acquisitions in the last year and a half at very good prices to add to their existing assets.

The company has a clean balance sheet and day rates continue to trend higher.

Shares are trading at a large discount to the replacement cost of the OSV fleet and day rates need to go much higher to incentivize newbuilds.

Shares of Tidewater are up more than 30% after a 6% pop on Q1 earnings, and they still have a significant margin of safety.

Yesterday I wrote about Transocean RIG 0.00%↑ , a large company in the offshore rig sector. Today I’ll be writing on Tidewater TDW 0.00%↑ . They are also technically in the offshore sector, but they own offshore service vehicles (OSVs) instead of the larger drilling rigs. Tidewater is the largest player in the OSV market, and they have made two acquisitions in the last couple years to grow their asset base. Before going into Tidewater’s acquisitions from the last couple years, I want to give some additional context on the OSVs and the differences from the rigs.

OSVs

Rigs are the assets responsible for extracting oil, but they don’t just operate on an island. They all require OSVs to service a variety of functions. This includes platform supply vessels (PSVs), anchor handling towing supply vessels (AHTSs), crew boats, offshore tugs, and specialty vessels for other functions. In my opinion, there is a lower barrier to entry for boats compared to rigs, but Tidewater has significant market share in the OSV space.

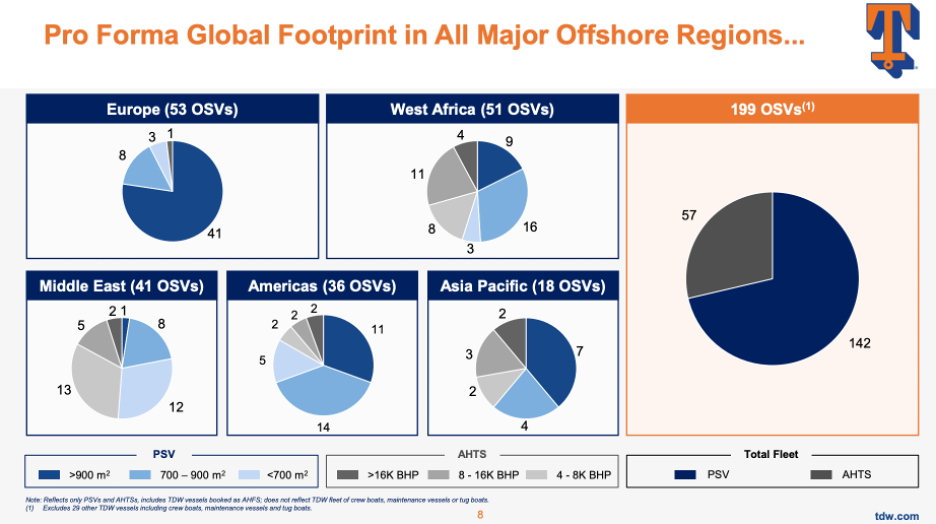

I’m paraphrasing from the podcast here, but for every rig, you need roughly 4 OSVs. Tidewater’s fleet is predominantly PSVs (142 boats) and AHTSs (57), but they also have 29 boats that fall in the other categories after their recent acquisition. They have assets all over the world serving all the major offshore locations. The average age of Tidewater’s fleet is around 11 years old, which compares favorably to the competition. Tidewater’s recent acquisitions have set them up well for the upcycle, and I think they got a steal on both deals.

Acquisitions: Two Heists In As Many Years

Tidewater’s first recent acquisition occurred in March 2022, when they announced the purchase of Swire Pacific Offshore Holdings for $215M ($42M in cash) and closed in April 2022, allowed Tidewater to add 50 OSVs. More recently, management announced the acquisition of 37 OSVs from Solstad Offshore. The acquisition is expected to close by the end of Q2 as long as they can get regulatory approval. To fund the acquisition, the company will be using a combination of their new three year, $325M credit facility, new debt financing, and cash on hand. They agreed to pay $577M in cash, which I think will look like a steal in a couple years.

Above is a quick overview of what Tidewater’s assets will look like after the Solstad acquisition. Most of the newly acquired ships are in Europe, but if you are as bullish on offshore as I am, adding 37 ships at about one third of the estimated replacement cost is just another reason to be bullish on Tidewater. Like I have mentioned in the last couple posts, the offshore sector is cyclical, and I think these well-timed acquisitions will prove to be very profitable for Tidewater and its shareholders.