Portfolio Update

A Look At Offshore Earnings Season, A Headline Overreaction On Petrobras & One Stock I'm Planning To Sell

Instead of the usual Videos of the Week post, I wanted to write an update on some recent news on some of the stocks in the portfolio. There were plenty of earnings updates, a couple notable insider transactions, and news from Petrobras that caused a decent selloff last week. I already wrote up my thoughts on the coal stocks, so I will primarily be focused on the rest of the portfolio. I did want to briefly mention Peabody Energy BTU 0.00%↑, since Elliott Investment Management has continued to sell their position. They now hold just over 5.9M shares as of Friday (3/1), which is down more than 2M shares in two weeks. Now let’s talk about the offshore sector.

Signs Of Life In The Offshore Sector

I have talked about the offshore sector for awhile, but I wanted to write a quick update on the stocks I own after their recent earnings releases. Like I have talked about before, I think the deepwater day rates might take longer to increase than OSVs and jackups. I wrote about the bombed out sentiment across the space in January, but if oil starts to perk up, I think stocks across the sector could be set for a nice run.

The Offshore Sector: Weak Sentiment To Start 2024

Summary Sentiment around energy and the offshore sector in particular has been down in the dumps, and I think it is a good time to be looking to add exposure to the sector. Oil prices still can’t catch a bid, despite conflict in the Middle East spreading beyond Israel/Gaza, and Yemen and the Red Sea, along with the Bakken production being down significantly due to freezing weather over the last couple weeks.

Tidewater

Tidewater TDW 0.00%↑ has basically sidestepped the pullback from some of the other offshore names, and the market obviously liked their earnings report last week. Shares were up more than 10 bucks a share (more than 14%) on Friday, hitting all time highs. Any time you see a move like that, a short-term pullback is probably right around the corner, but I think the long-term bullish thesis still looks fantastic. OSV day rates continue to trend higher and Tidewater is well positioned for that trend.

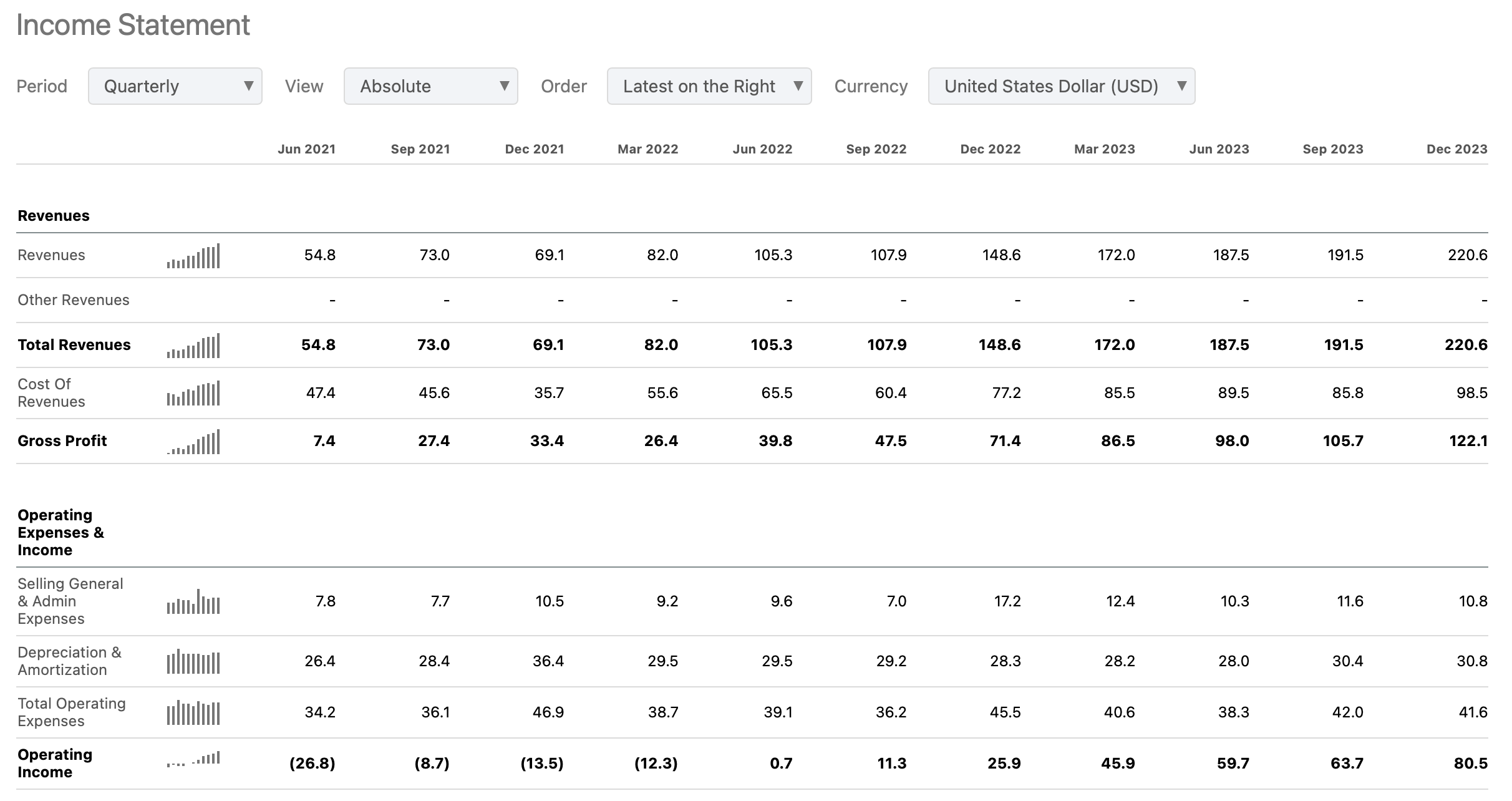

The highlight from the earnings call was the buyback program in my opinion. They bought back $35M in November and December, which was the maximum amount allowed under their current debt covenants. They authorized a new buyback program of $48.6M this quarter (again the maximum amount allowed under current debt covenants). They will be updating the buyback program on a quarterly basis, but I’m looking forward to continued buybacks this year for Tidewater. If you look at the quarterly trend of revenue and income over the last couple years, it looks similar to the picture of Borr’s quarterly results below.

Transocean

I don’t have much to say about Transocean’s RIG 0.00%↑ earnings call, except that it seems like they have a couple deals in the pipeline as far as new contracts. We will have to wait and see, but “stay tuned” shows up on the conference call transcript three times, so I wouldn’t be surprised if we see some new contracts in the next couple months. They still have the best deepwater fleet in my opinion, but they still have work to do as far as the leveraged balance sheet. RIG shares are notoriously volatile, but I think the underlying business is still headed in the right direction. Someone on Twitter pointed out that shares typically have larger moves in both directions than other stocks in the sector. When oil is heading higher and the offshore stocks are rallying, Transocean will usually outperform. When the opposite happens, Transocean typically sells off harder.

I like to think I’m more patient than a lot of investors, but I would be lying if I said I wasn’t a little bit frustrated with shares going from above 8 bucks last fall to where we are today. We recently had some insider buying show up, and the optimist in me is hoping that we have found a bottom. Shares were up more than 8% on Friday after news of a 1M share insider buy came out Thursday night. I was wondering if/when we would start seeing some insider buying on these stocks after the recent pullback, but I think shares are very cheap right now.

Borr Drilling

Borr Drilling BORR 0.00%↑ shares got smoked about a month ago after news that the Saudis were halting plans to expand their production capacity. They have bounced back a bit since then, but I still think shares are absurdly cheap right now. If I was looking to add to any of my offshore positions, Borr would be my pick (unless you want to speculate on Valaris warrants). Jackup day rates continue to grind higher, and I think Borr is set to become a cash cow over the next couple years.

There was a lot to like from the earnings call, but as long as day rates continue to trend higher, revenue and profit is going to trend up and to the right. The other thing worth mentioning is that they announced they would be borrowing an additional $200M last week. I’m assuming most of that will go towards paying for the 2 new jackup deliveries, which should be sorted by the end of this year. They have another dividend of $0.05 on the way, and I’m curious to see how aggressive they are with their $100M buyback authorization. We will have to wait until the next quarterly report to see on that, but I think shares are an absolute bargain near $6.00.

Valaris

Like Tidewater, I’m expecting more buybacks from Valaris VAL 0.00%↑ in 2024. They bought back $200M worth of shares in 2023, and boosted their existing buyback authorization from $300M to $600M. They are exposed to jackups as well as deepwater, and like Borr, shares got whacked on the news out of Saudi Arabia last month. Shares have bounced a bit since then, but I still think you can buy shares of Valaris for pennies on the dollar right now if you have a three to five year time horizon. For speculators, the Valaris warrants look very attractive to me, but I think the shares, like other stocks in the sector, are very cheap today.

South American Energy

I also wanted to spend some time on the South American energy stocks that I own, as they have been in the news over the last couple weeks. There have been some positives, like the announcement of a new dividend from Frontera Energy, and some negatives, like the news article about Petrobras potentially shifting towards renewables. We got earnings last week from Ecopetrol, with earnings on tap this week for Frontera and Petrobras.

Frontera Energy

Frontera Energy has been an eyesore in my portfolio for awhile (I should have just bought more Petrobras), but there have been a couple positive developments with one of their recent announcements. It’s a small speculative position, but they announced they would be paying out a small quarterly dividend ($0.0625 CAD per share, or 3.1% yield annualized) and have been buying back stock. They have repurchased 508,000 shares for approximately $3M as of 2/14. The buyback authorization is for just under 4M shares. They report earnings later this week, so I’m hoping for a positive update on their offshore block in Guyana, but I’ll be giving this one some more time as long as they continue to buy back shares and pay dividends.

Petrobras

Petrobras PBR 0.00%↑ has been the magic money tree over the last 12 months (knock on wood), and the dividends will continue to flow in my opinion. They also report earnings later this week, but shares dropped last week after the CEO discussed a shift towards renewables in a recent interview.

Latin America’s biggest oil company will be more cautious about issuing blockbuster dividends as it moves to become a renewable energy powerhouse, Petrobras Chief Executive Officer Jean Paul Prates said in an interview.

In 10 years about half of Petrobras’s revenue will come from wind, solar and renewable motor fuels — and the company is gearing up to make acquisitions as early as this year to propel the shift, Prates said in a wide-ranging interview. The Brazilian producer also needs to spend heavily on oil exploration at home and abroad to guarantee that it will continue pumping crude for decades.

“We need to be cautious. Shareholders will understand,” Prates said from Bloomberg’s office in Sao Paulo, when asked about an extraordinary dividend payment. “I would be more conservative than aggressive. We are in the middle of this great decision of becoming an oil company in transition.”

Actually, shareholders will not understand why the company would shift that heavily towards so-called renewables. Investors don’t own Petrobras so they can get taken for a ride on solar or wind. We own it for the massive offshore reserves, potential for production growth, and a dividend that dwarfs the payouts of most energy companies based in the US. They will be spending a lot on Capex in coming years, but I’m expecting most of that will go towards the traditional energy side of the business. I think talk of a shift towards renewables is just that: talk. Until we see an actual strategy shift, I don’t see any reason to sell my shares now. That might change, but I’m sure we will get an update this week with earnings.