Vornado Realty Trust: A Contrarian Opportunity In Office Real Estate

Can I Interest You In Manhattan Office Real Estate?

Summary

Vornado is a $4.3B office REIT focused on Manhattan real estate. Shares have had a rough couple of years due to government lockdown policies that created the work from home boom.

Sentiment, while it has been improving over the last couple months, is still terrible on office REITs. If you need any convincing, just look at the recent New York Magazine cover.

Below I do a deep dive on Vornado’s balance sheet, talking about the assets, like Penn Station and the stake in Alexander’s. I also talk about the large amount of debt on the balance sheet, which doesn’t have any significant maturities until 2025.

Vornado’s common stock recently cut the dividend to zero, but announced a $200M buyback. Investors looking for current income might want to take a look at the preferred shares.

I think Vornado shares have significant upside, and their experienced management and trophy assets separate them from the other office REITs.

I mentioned Vornado VNO 0.00%↑ in the podcast of the week post on Monday, but today will be a deep dive on why I bought shares of Vornado a couple months ago. Vornado is a REIT with a $4.3B market cap that is primarily focused on Manhattan class A office real estate. While the government lockdowns over the last couple years created a boom for working remotely from home, it also created one of the worst environments for office real estate possibly ever. I don’t think work from home is a long-term solution for most people, careers, or businesses, but I could see a hybrid environment becoming more common in coming years. If you think full time work from home is here to stay, then Vornado probably isn’t for you. However, investing in Vornado is very different from buying a mediocre office building in a suburb.

The trope with real estate is location, location, location, and it definitely applies with Vornado. Their main focus is New York, but they have a couple assets in Chicago and San Francisco as well. While AI has certain sectors of the stock market ripping higher in 2023, the office real estate sector has been a dog, for good reason. There are plenty of players in the sector with overlevered balance sheets, mediocre assets, and other issues. I do think there are several things that make Vornado a diamond in the rough, which I will discuss in detail below. I will start with the things that create a contrarian investment opportunity like Vornado: a large decline in price and bombed out sentiment.

Bombed Out Sentiment

If you look at a 10 year chart of Vornado, it’s not pretty. Shares spent most of the time between $60 and $80 until world paused in March 2020. They bottomed near $30 and rebounded to $50 in 2021, and it has basically been downhill from there. Sentiment around commercial real estate, and more specifically office, has been brutal in 2023, but I think that the selloff is overdone. Part of the panic was due in part to the Silicon Valley Bank blowup and investors realizing in the aftermath just how much commercial real estate is sitting on bank balance sheets across the US.

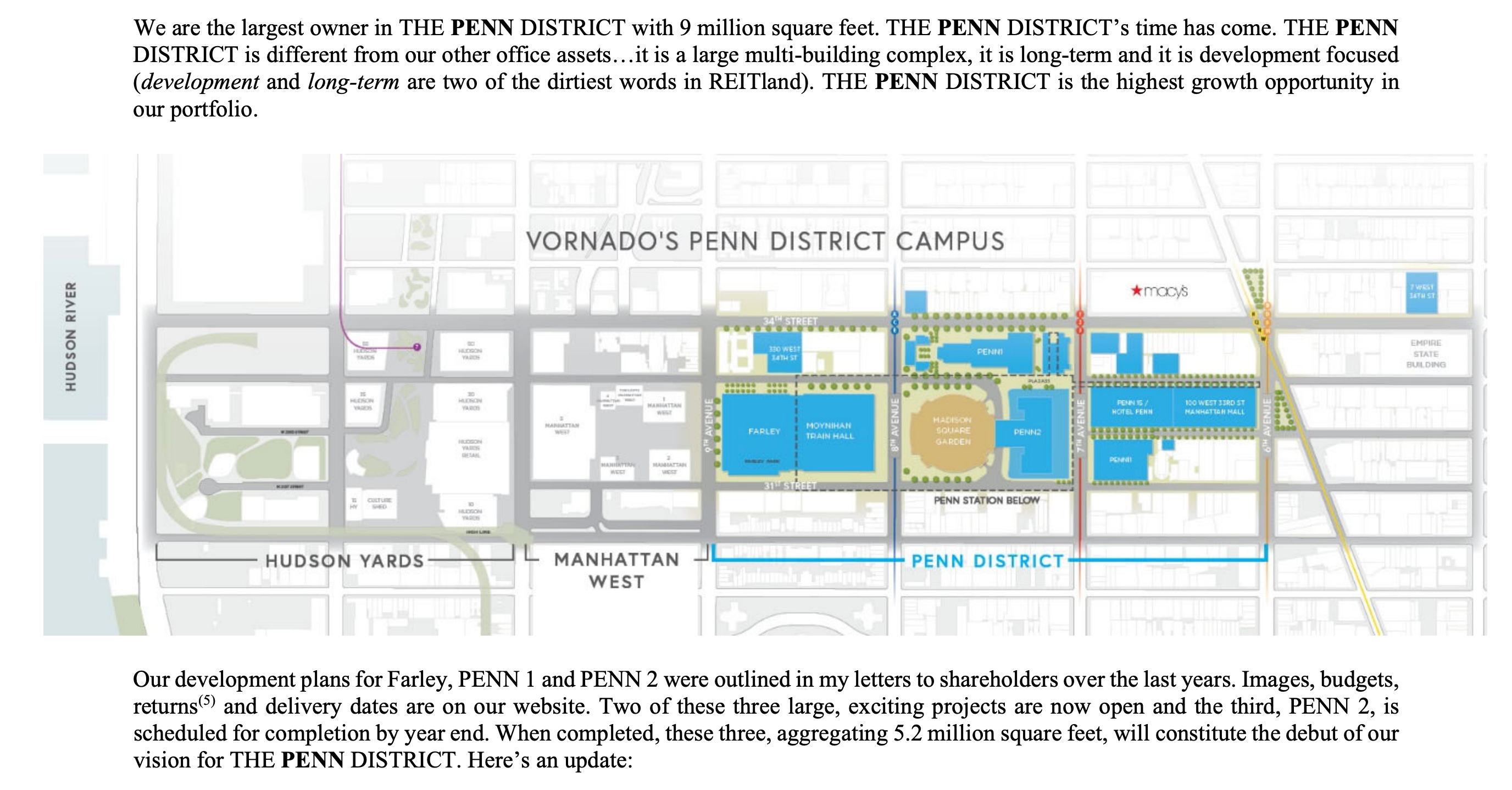

Shares of Vornado have traded below $13 in March and May, but they have rallied over the last couple months and now trade for just over $20. The nonstop negative headlines from office real estate seem to be slowing down, but sentiment is still pretty bad on office real estate. If you don’t follow the news cycle, below is a a recent cover of New York Magazine (7/17/23). If you look at the top left, 1 Penn PLZ (or Penn 1) and 2 Penn PLZ (or Penn 2), are actually Vornado buildings that are currently being redeveloped.

They are getting close to finishing up the redevelopment on those buildings, but this brings me to the the most important part of the bull case on Vornado: the assets owned by the REIT.

Assets

Vornado’s balance sheet is a puzzle with a lot of pieces, but once you pull it apart, it shows a lot of trophy assets and a debt ladder that should be able to weather what could be a weak stretch for the economy. If you take another look at the picture above, the building you see in between Penn 1 and Penn 2 is Madison Square Garden.

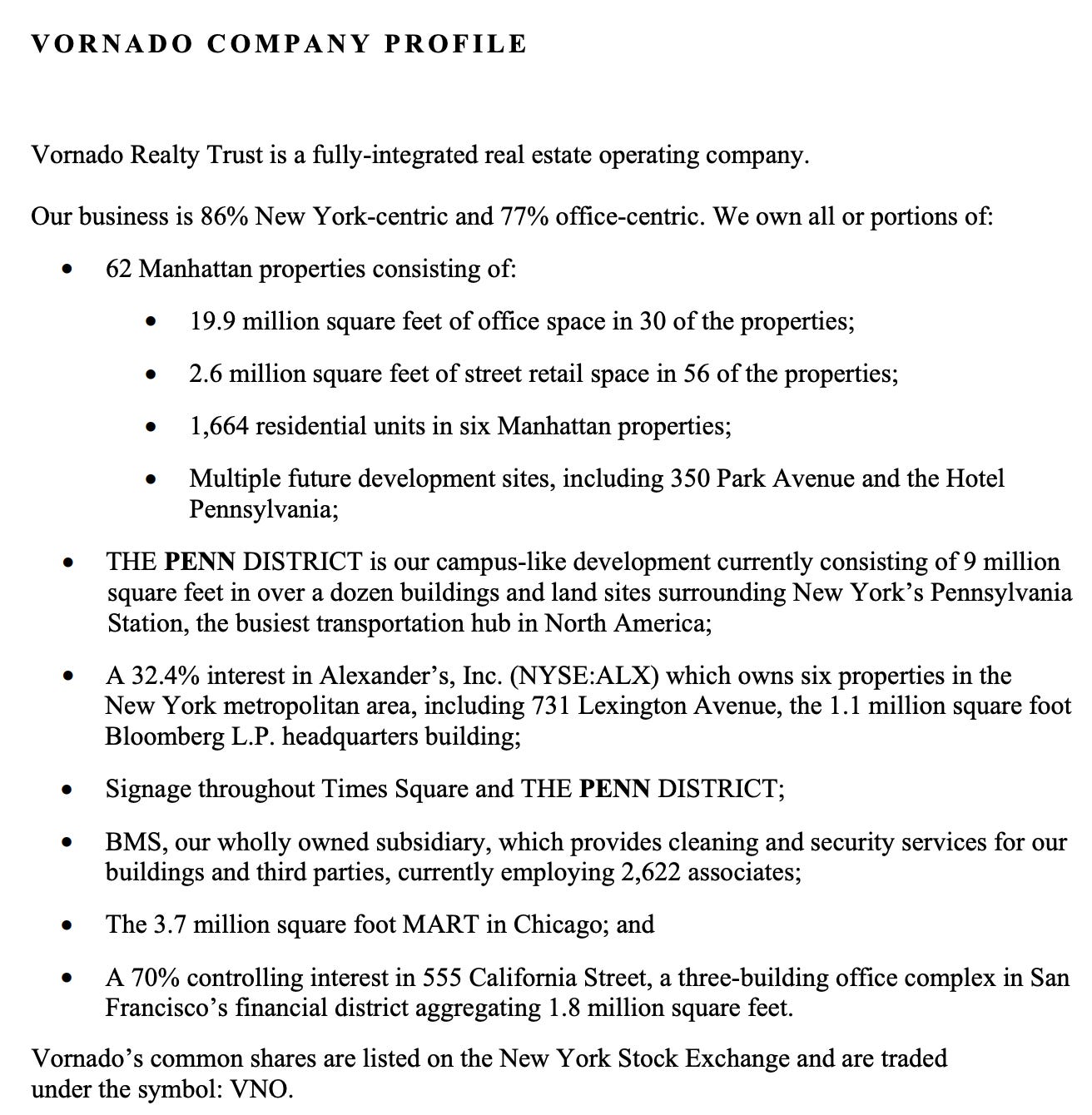

If you are interested in reading the letter, I have included a link here: 2022 Letter From The Chairman (and CEO), Steven Roth. Vornado’s assets in the Penn District are going to be very important to the future of Vornado, and the development should be wrapping up this year. To give a brief summary of the rest of Vornado’s assets, I will include another page from the Chairman’s Letter.

Investors have gone back and forth about what the land and buildings are worth, but I want to spend some time talking about some of the other assets on Vornado’s balance sheet. Some of these values will be updated next week with Vornado’s Q2 earnings report, but most line items don’t see dramatic changes on a quarterly basis. As of March 31, Vornado had $891M in cash and equivalents, $143M in restricted cash, and $277M in Treasury Bills. On top of the $1.3B in short-term liquidity, Vornado also has $2.67B in investments in partially owned entities, one of which is another New York REIT, Alexander’s.

Alexander’s

Vornado also owns a 32.4% stake in Alexander’s ALX 0.00%↑ (current market cap of $963M, which values Vornado’s stake at $312M). Alexander’s trophy asset is 731 Lexington Avenue, which is Bloomberg’s headquarters. That is their only office asset, but they also have Alexander’s Apartment Tower, with the rest of the portfolio focused on retail. Alexander’s has paid a quarterly dividend of $4.50 since the first quarter of 2018, so I wouldn’t expect any dividend hikes there, but Vornado will be receiving approximately $30M in dividends from Alexander’s over the next twelve months. If the thesis on New York real estate extends to Alexander’s, I think Vornado will continue to receive dividends and the value of their stake will likely appreciate over the next couple years.