Valaris: Worth A Small Speculation

Why The Valaris Warrants Are An Asymmetric Bet On The Offshore Sector

Summary

Valaris is an offshore company with a market cap of $4.4B.

I prefer other management teams in the sector for several reasons.

Despite that, I do think the Valaris warrants provide an interesting setup with the potential for asymmetric returns.

It is my smallest position in offshore, but I am considering adding to the position just like I am with Transocean and Tidewater.

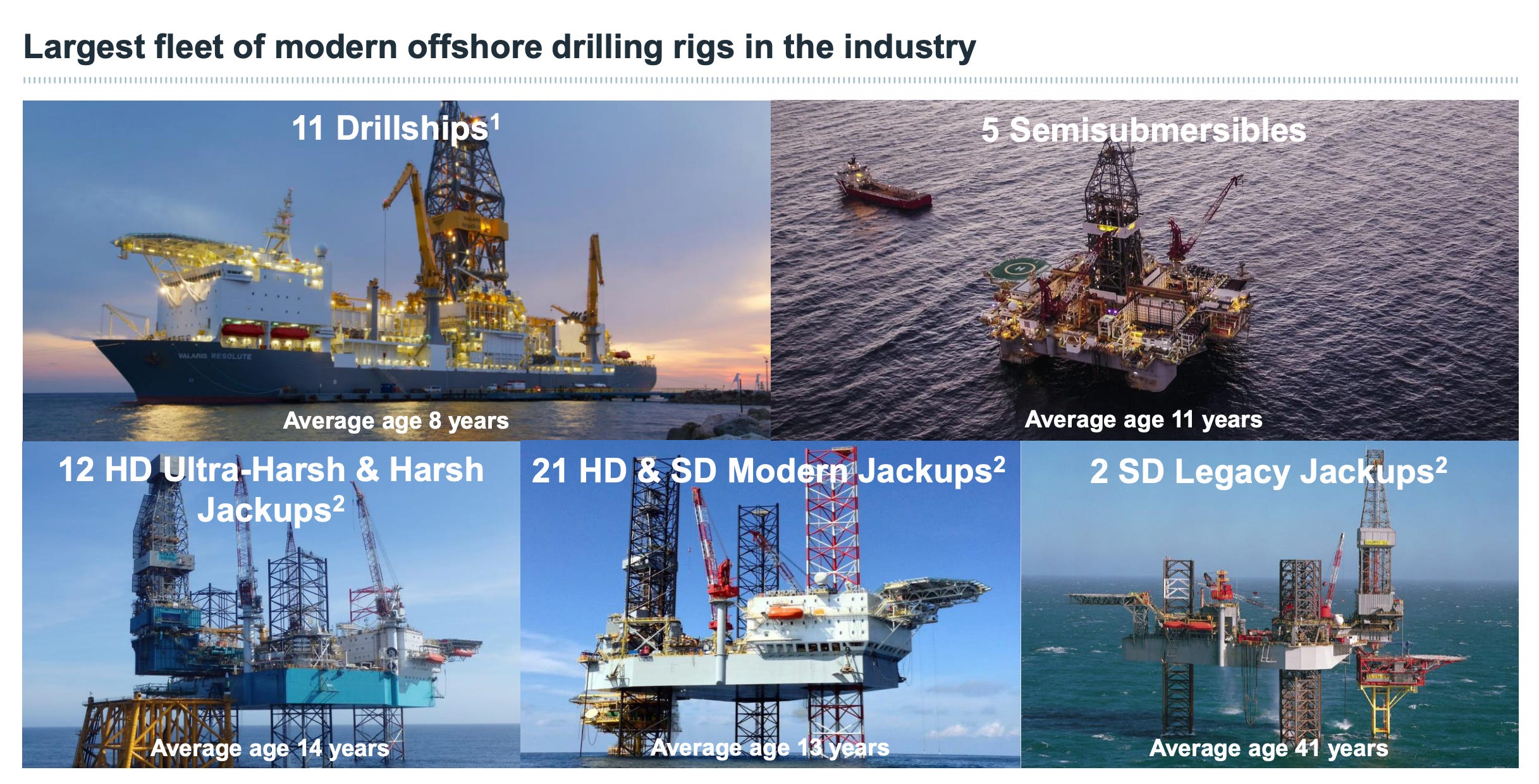

Overview

Today’s post is going to be shorter, but I want to give a brief summary of Valaris, which is my last position in the offshore sector. This position is much smaller than Transocean and Tidewater, but I own a tiny Valaris warrants position in my retirement account, separate from my main brokerage account. To sum up my thoughts on Valaris, the company will be a beneficiary of the same tailwinds that the rest of the offshore sector, but I’m not a huge fan of management. They have made several missteps in the last couple years, and I think Transocean is a better option for investors despite the leveraged balance sheet.

Management

There are a couple things from the podcast that I included on Monday’s post that I want to reiterate today. Judd Arnold, the guest on the podcasts of the week, views Valaris as the company with the best assets but the worst contracting position in the sector.

Valaris is trading at a steeper discount to replacement cost than Transocean (you can see the graph from my post on RIG), but I would still rather own RIG. After coming out of bankruptcy, the company is run by distressed debt investors. I would strongly recommend that readers check out this letter (link here) which discusses some of the things which highlight issues with Valaris.