Frontera Energy: A South American Speculation On Offshore Exploration

Frontera's Corentyne Block Could Lead To Huge Upside For Investors

Summary

Frontera Energy is a South American energy company with a market cap of $730M and is dual listed on the American and Toronto Stock Exchange.

The company already has existing operations in Colombia and trades at a P/E of 5x.

The biggest reason to own Frontera is the exploration of the Corentyne offshore block in Guyana.

They own 76% of CGX Energy, which is developing a port on Guyana and owns a 32% working interest in the Corentyne block. This brings Frontera’s interest in the block to 92%.

I view the company as a speculative holding, but if the offshore exploration is successful, Frontera is deeply undervalued today.

Today we are staying with the South American energy companies, but this one is much smaller than Petrobras PBR 0.00%↑ or Ecopetrol EC 0.00%↑. Frontera Energy is a small cap company that primarily has operations in Colombia, but they are also exploring an offshore block of Guyana. Neighboring areas of Guyana have proven to be massive offshore resources, including the Stabroek block operated by Exxon Mobil XOM 0.00%↑, with Hess HES 0.00%↑ as junior partner. Today I’ll bounce all over to discuss Frontera, but the biggest reason I own the stock is the exploration going on in the Corentyne offshore block in Guyana.

Existing Operations

Frontera currently has operations in Colombia (including a midstream segment) and small operations in Ecuador. Like any other energy company, the decline in oil prices has been a drag on results compared to last year. There are plenty of exploration companies looking for commodities, but Frontera’s existing operations (which you can buy at a cheap valuation), gives investors some downside protection while the offshore exploration effort could be a significant catalyst for shares.

Frontera has a valuation that looks cheap, with a price to earnings multiple between 4x and 5x depending on where you look. The share price in the short-term will be driven by news related to the Corentyne block exploration efforts, but if you think oil prices will head higher over the next couple years, Frontera’s existing operations will continue to be profitable. The company has no significant debt maturities until June 2025 and plenty of cash on the balance sheet, and they have been buying back stock at good valuations. If their offshore exploration efforts turn out to be successful, the current valuation will look like an absolute steal in a couple years.

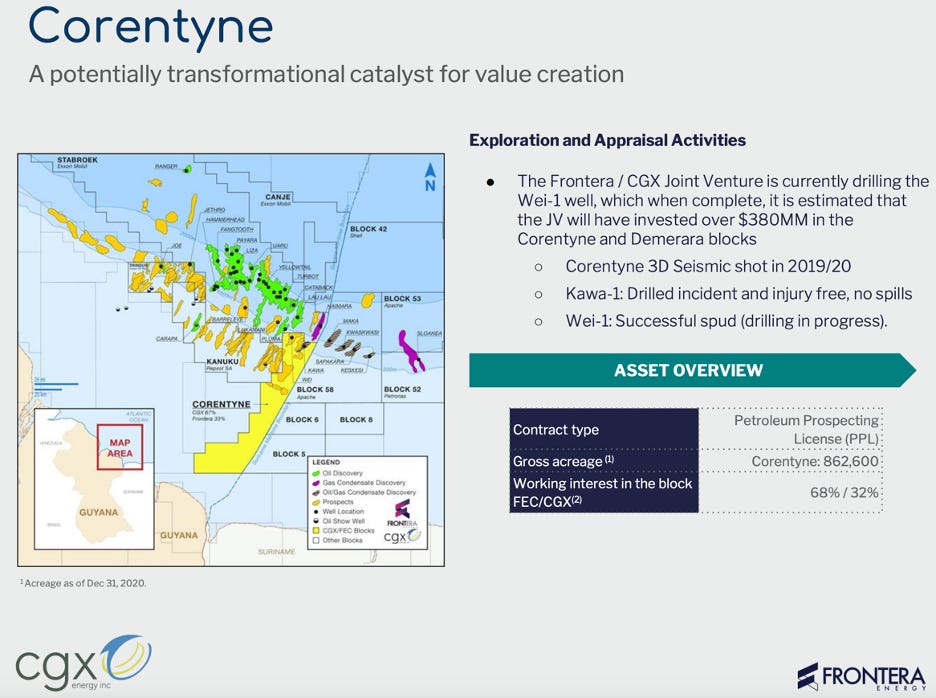

Guyana Exploration

For readers that aren’t familiar with Guyana and the offshore investment in the country, it has been one of the largest discoveries in recent years. Exxon Mobil (and junior partner Hess) are sitting on a black gold mine with the Stabroek block in offshore Guyana. They have already discovered 11B BOE (barrels of oil equivalent) and that could turn out to be conservative depending on how future exploration goes. If you are interested in some background on Hess and their block in Guyana, I have included links to a recent Seeking Alpha article and Hess' recent investor presentation.

The reason I started with the Stabroek Block is that the northern section of Frontera’s Corentyne block runs along the same fairway that has proven to be so lucrative for Exxon and Hess. Frontera is the operator of the block, with a 68% working interest. When you factor in their ownership of CGX Energy, their working interest is over 90%. It’s hard to know what the block is worth, but if exploration goes as planned, it could be worth multiples of Frontera’s current $730M market cap.

If the discovery proves to be commercial, chances are that Frontera (and CGX) will listen to bids from larger companies to come in and operate the block. If that happens, I think investors buying today will see very attractive returns. If you are a visual learner instead of a reader, I strongly recommend that interested investors go back to the Deep Diving Oil & Gas video from a couple weeks ago and skip to 1:38 mark. It is a great 30-minute summary of the bull case for Frontera and CGX Energy.