Borr Drilling: Premium Jackups With Catalysts On The Way

Borr's Leveraged Balance Sheet Provides Torque For The Offshore Bull Cycle

Summary

Borr Drilling owns a fleet of 22 premium jackups with two new builds on the way. Their jackups command a premium day rate compared to older jackups.

Like deepwater rigs, there is very little supply of jackups coming online, and many are set to be scrapped in coming years. The same bullish case for deepwater rigs can be made for jackups, with a lack of supply leading to a supply and demand mismatch, ultimately leading to higher day rates.

Utilization is at 93.9% for premium jackups and day rates have continued to increase. Borr’s contracting position opens up significantly over the next couple years, giving them torque to higher day rates.

Borr’s leveraged balance sheet might give some investors pause ($1.6B in total debt), but management has stated that their priorities are refinancing their 2025 debt, which should lead to dividends and/or buybacks. Both of these things could be catalysts for the stock in the next year or two.

The debt also means more upside potential in an offshore bull market. Borr’s recent operating results show the trend of higher day rates and improving profitability. I expect Borr to turn into a cash cow over the next three to five years.

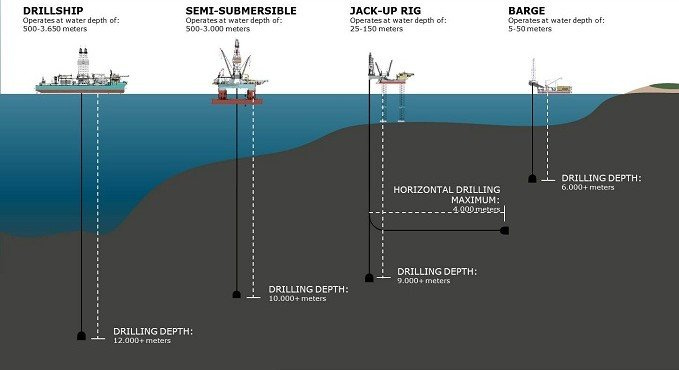

I have talked about the offshore sector in several posts, and it looks to me like a sector with a bright future on the horizon. Most of my focus has been on deepwater and OSVs, but today I will be focused on jackups. The reasons I’m bullish on jackups are basically the same as deepwater. There is almost no new supply of jackups being built, rising utilization which has led to rising day rates, and stocks in the sector with assets trading well below replacement cost. Below is a picture that shows the difference between the different types of offshore ships.

Borr Drilling BORR 0.00%↑ is pure play jackup operator, and like Transocean RIG 0.00%↑, they have a debt load that should provide leverage to the upside as the offshore cycle gets going. The debt creates some additional risk, but I think shares are a bargain today below $7.00. Investors looking for exposure to jackups with less balance sheet risk might want to take a look at Noble Corporation NE 0.00%↑ and/or Valaris VAL 0.00%↑. Both repaired their balance sheets coming out of the last offshore bankruptcy cycle, so there is less risk there financially, but I prefer Borr for my jackup exposure. If you want a refresher on my bull case for offshore, I have linked my post from May below. Many of the same points apply to jackups and Borr as well.

Offshore: Early Innings Of A Cyclical Upswing

Summary The podcasts of the week are focused on the offshore sector and companies that are well positioned for attractive returns over the next 3 to 5 years. The energy industry is cyclical, but offshore has very long cycles compared to conventional energy. The last peak was in 2014 and I think we are in the early innings of a cyclical upswing.

Since that post (May 8th), the price of oil and stocks in the offshore services sector have had a nice run. Transocean, one of my favorites, is up approximately 25% even after the recent pullback. Tidewater TDW 0.00%↑ is slightly off its highs, but it is up 50% since May. Noble and Valaris are up approximately 27% and 20%, respectively. I have been looking to buy some Valaris warrants recently, but I will save that for a short post next week. Borr has lagged the rest of the sector (going from $7.12 to $6.74 in the same time frame), and the last couple months has provided a nice pullback, with shares going from $8.90 on August 1st to $6.74 as I write this. While I think the long-term setup is brightest for deepwater rigs because I think the cycle could be longer, there is a place in my portfolio for jackups as this offshore cycle starts to run.

Borr Overview

Borr Drilling operates a fleet of 22 jackups, with 2 more jackups under construction that should be delivered in the next couple years. Right now, they are looking to accelerate delivery on the two jackups under construction (Vale and Var) from 2025 to late 2024.

Supported by our confidence in the jack-up rig market, we are in active discussions with Seatrium, formerly Keppel, for an expedited delivery of our rigs Vale and Var to August and November 2024, respectively. As we see significant opportunity to increase earnings with having these last two top-tier rigs available.

- Q2 Earnings Call

By Q4, they expect all 22 of their existing jackups to be in operation after they had a contract in Africa get cancelled in July. One of the things worth mentioning about Borr’s jackup fleet is that they are newer than a large portion of the jackup market, and the modern jackups command a significant day rate premium to older jackups. Like deepwater rigs, jackups are long-lived assets, and Borr’s fleet has an average age of approximately 6 years. The modern jackups have also seen slightly higher utilization, with modern rig utilization sitting at 93.9% while standard rig utilization is lagging slightly at 89.7%.

“Once utilization get to 80%, day rates start inflecting.” – Judd Arnold

I have seen a lot of chatter on financial Twitter from accounts focused on offshore about day rates across the offshore space, with some predictions for $500,000 for deepwater by the end of the year, and talk for $200,000 a day for jackups. If we don’t see a 500k day rate for deepwater in 2023, I’m confident that we will see it in 2024. I think we will see 200k for jackups in 2024 as well, but I’m not as confident because that would be a larger move in day rates. What I am expecting is that Borr (and other players in the jackup sector) will turn into cash machines as day rates continue to rise. So far this year, Borr has signed 7 new contracts at an average day rate of $163,000, and their contracting position opens up meaningfully over the next couple years.

Our current contract revenue backlog stands at 34.1 rig years for a total of $1.64 billion. This equates to an equivalent rate of $132,000 per day, which we believe to be industry-leading for jack-ups.

- Q2 Earnings Call